Resource Center

Educational articles, guides, calculators, and tools designed to help Texas homebuyers, homeowners, investors, and sellers make informed real estate and mortgage decisions.

Understanding the True Cost of Homeownership

The Real Costs, Risks, and Financial Responsibilities of Buying a Home

By: Justin Troy Cox

Published: June 4th, 2026

Homebuying, Homeownership

Estimated read time: 14 minutes

Whether you’re a first-time home buyer or a seasoned investor, the process of buying a home can range from being exciting and fun, to being utterly stressful and anxiety inducing. Many buyers spend countless hours excitedly shopping online for their dream home, and just as many hours anxiously thinking about monthly payments or whether they can afford a down payment. And just as many are surprised by the true long-term costs of homeownership after achieving their goal.

That monthly payment isn’t just your mortgage. It can also include a portion of your annual property taxes and homeowner’s insurance, both of which can change significantly over the years. And oftentimes, the costs of maintaining and owning a home are understated or even completely unaccounted for. Two homes that sell for the exact same price can have very different overall ownership costs.

Why is this? Homebuying is a complex process that has developed over an extended period to include industries that most people only interact with a few times in their lives. Even the most experienced investors are sometimes caught off guard by parts of the process. Industry professionals become adept with repetition and experience, and every one of them has transactions that stick with them.

For home buyers it’s not necessary to understand all of the system’s nuance, but it is important to have a baseline understanding of the financial responsibilities that come with homeownership. It’s my hope that in doing so, you’ll avoid an anxiety inducing or stressful homebuying process, or even worse, an experience that’s the source of future financial hardship. Let’s begin by looking at some common mistakes that home buyers make:

Mistake #1: Lack of Realistic Expectations

Home prices reflect relative scarcity. People want to live near amenities they enjoy, they want perfect weather, and they want a home that is comfortable, modern, and that reflects their desired lifestyle. Parents want to be near the best schools for their children. Buyers want all of this, and preferably they want it to be as close to free as possible! Their demands are many, and homes that check all of the boxes are scarce, and high prices reflect that.

A person who makes few tradeoffs is likely to pay more for a home. Real Estate Agents understand this and endeavor to help their clients buy a home they’ll love, while longer-term financial implications may receive less attention during the initial shopping process.

Mistake #2: Too Much Focus on the Purchase Price

Many home buyers (and their agents) focus solely on the price, when in reality the monthly payment is the key to qualifying for financing. Two homes with identical prices can have significantly different monthly payments and ongoing costs of homeownership based on differences in property taxes, homeownership insurance, and characteristics of the home. That $400,000 prequalification can really be $380,000 for one home, and $425,000 for another home.

Mistake #3: Misplaced Trust

Buyers, often for good reason, do not trust the professionals they’re working with. It’s quite common for buyers to ghost Realtors or Lenders who give advice or guidance that is contrary to their (potentially unrealistic) expectations and/or desires. Meanwhile, it’s just as common for buyers to accept guidance from trusted family or friends who are not experts and who base their guidance on anecdotal information or situations that they misunderstood.

A Better Approach

My recommendations for home buyers are simple: Setting realistic expectations for your purchase upfront by budgeting earnestly for your monthly payment and upfront costs is the first key. From there, understanding monthly payment components and transaction costs will help you balance the things you desire in a home with the financial reality of homeownership. It’s also important to understand the ongoing costs of homeownership after you achieve your goal. Lastly, it’s important to work with the right experts to help make your dream a reality.

Setting Realistic Expectations

Realistic expectations start with three questions: First, how much can I really afford as a monthly payment? How much can I afford to pay upfront for my down payment and closing costs? With these in mind, how much can you realistically save for future maintenance, repairs, or other unexpected expenses associated with homeownership?

The answers to these questions depend on your specific situation, but a good general rule of thumb is to target a monthly payment that’s less than 1/3rd of your take home pay. This can vary depending how much “residual income” – money available after paying your mortgage – you have.

A couple making around $60,000 annually will take home approximately $8,000 per month after taxes. A third of this is $2,666.40, which leaves them a healthy residual income of $5,333.60 for their living expenses and other bills.

This is similar to qualifying for a mortgage, but lenders can often qualify you for more because similar calculations they perform are based on your pre-tax income. For example, the FHA mortgage program caps a person’s mortgage payment at 47% of their pre-tax income. For this same couple earning $60,000 each ($120,000 annually), the FHA program allows a monthly payment up to 47% of their $10K monthly pre-tax income before accounting for their other debts. That’s $4,699.99 – a tremendous difference!

Upfront Costs (Down Payment, Closing Costs, and Prepaid Expenses)

When it comes to upfront costs, savings is the key. If you don’t have savings, you must consider if and how you can consistently save. If you do have savings, you must consider how much you can afford and where you’ll source funds. If you don’t have savings sufficient for your upfront costs, costly tradeoffs must be made. You could use a down payment assistance program, but these often come with higher interest rates or other longer-term restrictions on ownership or ability to refinance.

For closing costs, the seller, your agent, or your lender can contribute towards these, but that money comes from somewhere. Sellers typically pay real estate commissions, so having the seller or your agent help pay costs often means that you’re indirectly adding these costs to the price of the home. On the other hand, if the lender helps, your interest is likely to be higher.

A buyer with savings doesn’t have to make these tradeoffs. They’re able to negotiate a better price, better mortgage terms, and their payments are lower. The question for them is whether they should put more down or if investing offers a better return, or if they should preserve or maintain their emergency fund.

Your Emergency Fund

A good rule of thumb here is to have 6 months of all bills (including your new mortgage) saved up as an emergency fund. For that same couple from before taking home $8,000, if we assume 50% of their monthly pay goes towards bills, that’s $4,000 per month. A six-month reserve is $24,000. With these savings, they’ll be prepared for most unexpected expenses that arise. A hurricane damages their home? Whether or not to make an insurance claim is a point of debate instead of a necessity.

This amount varies for everyone. The real key is having an actionable plan to get there. Saving is always tough, but it’s tougher to live with stress and anxiety over an uncertain future, and it’s even worse to live with regrets after something bad happens.

Understanding Payment and Upfront and Long-Term Costs

My second recommendation for home buyers is to understand the components that make up your monthly payment and upfront costs. When buying a home, you may hear many unfamiliar terms. Expert level understanding isn’t 100% necessary so long as you understand the things that impact you most.

You’ll often see the acronym PITI with regards to your monthly payment. This stands for Principal, Interest, Taxes, and Insurance, and these categories represent the components that make up your mortgage payment. Let’s break these down:

Principal and Interest

Together, these represent your actual mortgage payment. Principal refers to portion that reduces your loan balance. Interest refers to the amount you pay the lender for loaning you money upfront. With a fixed rate mortgage, the principal and interest portion of your payment will not change. The amount is calculated using a process called amortization, which is a method of keeping your payment fixed while reducing the principal balance a bit each month while interest accrues until the loan is repaid.

Mortgages have front-loaded interest, so the portion of this fixed payment that goes to your principal balance will be very low at first, while conversely, interest payments are higher. But with each payment the principal portion increases while the interest paid decreases until the loan is repaid.

Taxes and Insurance

These refer to property taxes owed annually to local state, and municipal governments for public services, and to insurance to protect the home and the lender if you default on your mortgage. Taxes and insurance are only included in your payment when you have an “escrow account”, which is an account held by your lender that’s used to pay these items on a periodic basis.

Note: When applicable, mortgage insurance must be escrowed for. When you make your total payment every month, the tax and insurance portion is deposited into this account so the lender can pay for these expenses when they’re due on your behalf.

However, not all mortgages require an escrow account. Notably, VA and conventional mortgages allow you to “waive escrows” meaning you can pay these expenses on your own instead. This makes sense if you’re a person who has that emergency fund I mentioned before and who is comfortable with saving up for major expenses on a regular basis.

Waiving escrows means you can earn a return on your savings that you cannot when the lender holds onto these funds for you, and you also avoid periodic “escrow analysis” by the lender. Escrow analysis is a topic worth its own deep dive and is a common source of frustration for home buyers who often are not cognizant of property tax or insurance premium increases.

With property taxes, there are two components that determine what you pay – the tax rate, and the “assessed value”. This information is publicly available. (Just search [County] CAD, and you’ll likely find it.) Tax rates typically don’t change dramatically. What you owe is impacted most by changes to your assessed value. Therefore, it’s common for savvy homeowners to challenge the government’s value assessment (either themselves or with the help of their realtor or a specialist firm).

Homeowners Association (HOA) Dues

These are not included in your monthly payment or escrow account. When applicable, you must pay these on the payment schedule determined by the association. Normally, this is on an annual basis, but for townhomes, condos, or pricier HOA’s, these may be monthly. Your lender will consider this cost when qualifying you for your mortgage, so you may see the expanded PITIA acronym, which also includes the ‘A’ for Association Dues.

Upfront Costs: Your Down Payment

This is the portion of the purchase price that you pay upfront. Your lender finances the rest. Down payments vary depending on which mortgage program you use. The most common options are the FHA and conventional mortgage programs. The FHA program is backed by the federal government, while conventional mortgages are not.

First time home buyers can qualify for a 3% minimum down payment on a conventional mortgage, while the minimum is 3.5% down using the FHA program. VA and USDA mortgages do not require down payments. Each program can have down payment assistance programs layered on top to help with total upfront costs.

Closing Costs Overview

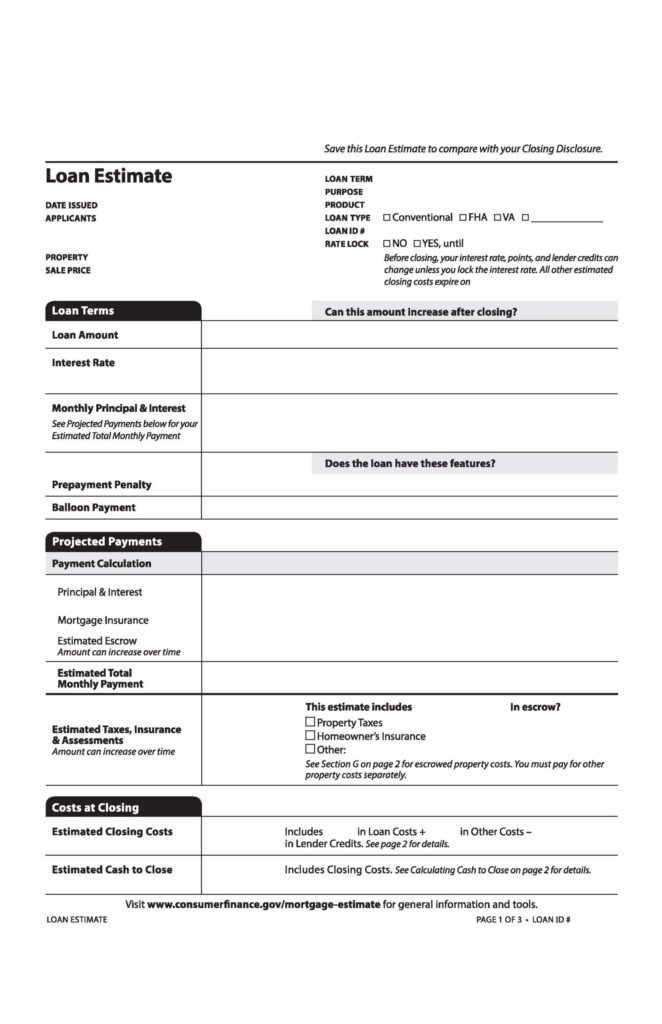

Home buyers often struggle to understand closing costs because the term broadly refers to the various costs associated with buying a home that are paid to multiple parties that provide necessary transaction services. By law, lenders must provide you with a Loan Estimate within three business days of receiving your mortgage application for a specific home.

The Loan Estimate separates costs into sections that I find are helpful in explaining costs. Section A includes costs paid directly to your lender. Section B includes costs paid to third parties your lender chooses for services they need to originate your mortgage. Section C is for other necessary services you’re allowed to shop for. Section D adds together Sections A, B, and C.

Section E includes taxes and fees paid to the government directly. I’ll cover Sections F and G when we discuss prepaid expenses next. Section H is for miscellaneous items that don’t cleanly fit into the other sections. Here’s a sample you can review. (Click to open it in a new window.)

Costs in Section A and B are directly controlled by your lender. Buyers often think less is more here but be careful. A lender who doesn’t disclose any costs here may make up for it by charging you a higher interest rate!

Section C generally includes the cost of a Survey (a map showing the boundaries of the property), and fees paid to the title company for title insurance and escrow services. In Texas, title insurance costs are regulated by the state and are directly tied to your purchase price and loan amount. Also, the title company requires a Survey to underwrite title insurance, so if there isn’t one, a new one will be required.

The things to look out for in Section C are the Escrow/Settlement Fee, which represents the title company’s fee for closing your transaction, and their miscellaneous charges. Some title companies have none. Others add charges for things ranging from title research to document preparation (i.e., printing the documents you’ll sign at closing), and so on.

In Texas, Section E fees are usually small because local government fees are minimal for recording the title transfer and mortgage in the public record. But some states include Transfer Taxes, which can represent a much bigger expense. Section H typically includes an optional “owners title insurance policy”, but when buying a home subject to an HOA, HOA charges will appear here, as well.

With newly built homes this can represent a sizable expense because new HOA’s usually charge a “capitalization fee” at closing which helps establish the initial reserves necessary for the operation of the HOA.

A Quick Note About Title Insurance

Homebuyers often ask about title insurance. Title insurance protects against title defects surrounding events that happened in the past. For example, if it’s determined after you buy a home that there was a fraudulent title transfer before you owned the home, your purchase could be undone.

Title insurance covers your loss with an “owner’s title policy” and the lender’s loss with a “lender’s/mortgagee’s title policy”. Your lender will almost always require a lender’s title insurance policy, but there are exceptions. But it’s always recommended that you purchase an owner’s title policy.

Prepaid Expenses Breakdown

These expenses are listed on Section F of the Loan Estimate and represent costs that are prepaid at closing. For example, your first annual homeowners’ insurance policy is normally the biggest expense here. But this may also include annual flood insurance, or a separate wind and hail insurance policy if your homeowners’ insurance doesn’t include lender required wind and hail coverage.

You’ll also prepay interest on your mortgage from your closing date until the day your mortgage begins. Mortgages always begin on the 1st of the month. If you close on May 31st, you’ll prepay one day of interest for May 31st, and your mortgage will begin on June 1st with your first payment on July 1st. If you close on May 15th, you’ll pay for May 15th through the 31st (17 days).

Prepaid Expenses: Initial Escrow Deposit

Section G is for the initial deposit into your escrow account. If you waive escrows, there won’t be any costs here. This section can be difficult to understand because the initial deposit varies based on your closing date and when the property taxes and insurance in your escrow account are due for payment. As an example, I mentioned before that your first payment would be July 1st if you close on May 31st.

With property taxes due on January 1st of each year, you’ll make 6 payments into the escrow account before they’re due. So, the lender will collect the other 6 months from you at closing to make up the full annual amount plus a two-month reserve – a total of 8 months for the initial deposit. For homeowner’s insurance, the first renewal is normally one year later. By then (May 31st) you will have made 11 months of payments into the escrow account, so the lender collects one month so they have the full annual amount plus an additional two-month reserve for a total of 3 months deposited.

From there, the lender reviews projected deposits and withdrawals from the account. They look for the lowest projected balance in the next 12 months. If that balance is more than your combined property taxes and insurance for two months, they give you a credit for the difference called an “aggregate adjustment”. This is because lenders can only maintain a two-month reserve by law. The goal of the reserve is to have sufficient funds in case taxes or insurance costs increase unexpectedly.

Long-Term Costs of Homeownership

When you purchase a home, you own an asset whose value will change based on supply and demand. I had a client who put down the minimum but had to relocate a year later. Higher rates meant lower buyer demand and a lower price, so my client did not have enough equity to sell without contributing additional funds. They had to rent their home instead – something they weren’t totally comfortable with that they would’ve preferred to avoid.

Historically, home prices have appreciated steadily, but historical performance is not a guarantee of future performance.

I recommended an emergency fund above. This is both a wise practice, and one that’s necessary for homeowners who bear the brunt of maintenance and repair costs on their homes. Deferring maintenance means less equity and leverage if you need to sell.

We also touched on property taxes and insurance, but it’s important to be aware that these costs typically increase year after year. Together, these represent the long-term ongoing costs of homeownership that you should account for when shopping for homes.

Working With the Right People

My final recommendation, and perhaps the most important one, is to work with the right professionals. I think many consumers are distrustful of salespeople because, in every industry, there are people who are experts in the psychological aspect of sales when they should be experts in their field first and foremost.

The best real estate agents and mortgage originators aren’t willing to sacrifice providing quality advice and expert guidance to generate more sales or commissions. The commissions they earn are the rightful byproduct of the value proposition they offer to their clients. Clients seek them out because they’re consummate professionals who provide valuable advice and guidance at a fair price and in an honest and transparent manner.

Closing Remarks

Buying a home will probably always feel a bit overwhelming because the stakes are so high financially and in terms of lifestyle for you and the people you care about. However, if you can approach the process with realistic expectations, a bit of knowledge about monthly payments and costs of homeownership, and with the guidance of experienced professionals, you’re more likely to achieve your goal while being confident in the decisions you’ve made and where you stand in the future.

Whether you work with both a Realtor or Loan Officer, or a team like ours that offers both, the most important thing is working with people who communicate clearly and who can help you understand the process and how the decisions you make impact you both today and in the long-term – not just someone who pushes you to sign on the dotted line.

Questions About Your Situation?

Every home purchase, refinance, and sale is different. Schedule a no-cost consultation to discuss your goals and options with our team. We’re more than happy to put our experience to work for to help.

A brief conversation can help answer your questions — there is no obligation to move forward.